Introduction

For decades, society has told us that success equals owning a home. “Get on the property ladder,” they say, as if buying a house is the only way to build wealth. But what if I told you that following this advice blindly could hold you back from achieving true financial freedom?

The truth is, you don’t need to own a house to build wealth. In fact, with the right financial system — like the 65-25-10 rule — you can generate passive income, gain freedom, and live life on your terms without being shackled to a 30-year mortgage.

In this post, we’ll break down:

- Why homeownership is not the only wealth-building strategy.

- What the 65-25-10 rule is and how to apply it.

- Real-life examples and calculations comparing buying vs. investing.

- How to use opportunity cost to your advantage.

- The step-by-step roadmap to financial independence.

Let’s dive in.

The Myth: Buying a House Equals Wealth

Why Society Pushes the “Property Ladder”

We grow up hearing that renting is “throwing money away” and that we need to buy a house as soon as possible. This belief is deeply ingrained because, for past generations, real estate was a forced savings plan. Monthly mortgage payments built equity, and over decades, homes appreciated in value.

But times have changed. Housing prices in many cities have grown far faster than wages. For example, in Toronto, the average home price in 2017 was $730,000. By 2023, it had jumped to $1.1 million — outpacing salary growth by a wide margin.

Meanwhile, maintenance costs, property taxes, interest rates, and hidden expenses eat into that “investment.” Owning a house isn’t just a purchase; it’s a lifestyle cost.

Real-Life Example: Buying a House vs. Investing

Let’s run the numbers.

- Imagine you buy a condo for $500,000 in 2017 with a $50,000 down payment.

- Fast forward 8 years: your property grows 10% in value → now worth $550,000.

- That’s a $50,000 gain on paper.

But let’s not forget the costs:

- Mortgage interest (~$100,000+ over 8 years).

- Property tax (~$2,500/year = $20,000 total).

- Maintenance & repairs (~$2,000/year = $16,000 total).

- Insurance (~$1,000/year = $8,000 total).

👉 Net gain after costs? Much smaller than $50,000.

Now compare that with investing your $50,000 down payment into the S&P 500 in 2017.

- The S&P 500 nearly doubled between 2017 and 2023.

- That same $50,000 could now be worth $90,000–$100,000+, without the stress of leaky roofs or rising property taxes.

📊 Lesson: Buying a house isn’t always the “best investment.” Sometimes renting + investing makes more financial sense.

Introducing the 65-25-10 Rule

So if owning a house isn’t the only path, what is? Enter the 65-25-10 rule — a simple, powerful money framework.

The Breakdown:

- 65% – Essentials

- Cover your core living costs (housing, utilities, food, transportation, debt minimums).

- 25% – Fun & Lifestyle

- Travel, dining out, hobbies, entertainment — guilt-free spending.

- 10% – Future You

- Savings, investments, and extra debt payments.

This rule ensures you live comfortably without neglecting your future wealth.

Why the 65-25-10 Rule Works

- Balances needs and wants → You don’t feel deprived.

- Automates wealth building → 10% consistently invested grows massively over time.

- Scales with income → Works whether you earn $50K or $500K.

Real-Life Calculation: The Power of 10%

Let’s say you make $60,000/year after taxes.

- Essentials (65%) → $39,000/year

- Fun (25%) → $15,000/year

- Future (10%) → $6,000/year = $500/month invested

Now, invest that $500/month in an index fund like the S&P 500 (historical average 8% return):

- After 10 years → $91,000

- After 20 years → $275,000

- After 30 years → $680,000

🔥 Just by consistently following the 65-25-10 rule, you can build a six-figure portfolio — even if you never buy a house.

Step 1: Build Your Peace of Mind Fund

Before investing, create a 1-month emergency fund.

- Example: If your living costs are $3,000/month, save that first.

- Why? Because financial emergencies happen — and stress-free money is powerful.

Step 2: Pay Off High-Interest Debt

Credit card debt at 20% interest can destroy your wealth.

- If you carry $10,000 in debt at 20% interest, you pay $2,000/year just to service it.

- That’s like pouring water into a leaky bucket.

Pay these off first before heavy investing.

Step 3: Build a Larger Emergency Buffer

Next, save 3–6 months of living expenses.

- Single with stable job → 3 months.

- Family with kids, mortgage, unstable income → 6 months.

Example: If your expenses = $3,000/month, your buffer should be $9,000–$18,000.

Step 4: Start Investing

Now comes the wealth multiplier: investing.

Where to Start:

- Employer retirement plan (401k / pension match = free money).

- Tax-advantaged accounts (IRA, Roth IRA, TFSA, ISA).

- Low-cost index funds (e.g., S&P 500, FTSE 100).

Why Index Funds?

Instead of betting on one stock, you own hundreds of companies. Historically, index funds return 8–10% annually — enough to double your money every 7–9 years.

Opportunity Cost: The Hidden Killer

Every dollar you spend has an opportunity cost — what it could have earned if invested.

Example:

- You buy a new iPhone for $1,200.

- If invested at 8% for 30 years, that money becomes $12,000+.

- 📱 That phone actually cost you $12K in opportunity cost.

Passive Income from the 65-25-10 Rule

By sticking to the 10% investment habit, you can create passive income streams:

- Dividends → Companies pay you for holding shares.

- Index Funds Growth → Capital appreciation builds wealth.

- Side Hustles → Invest profits into assets instead of liabilities.

Over time, this creates a snowball effect: your money works harder than you do.

Money Traps to Avoid

1. Lifestyle Inflation

Earning more? Don’t upgrade your car, phone, or wardrobe instantly. Keep expenses steady and invest the difference.

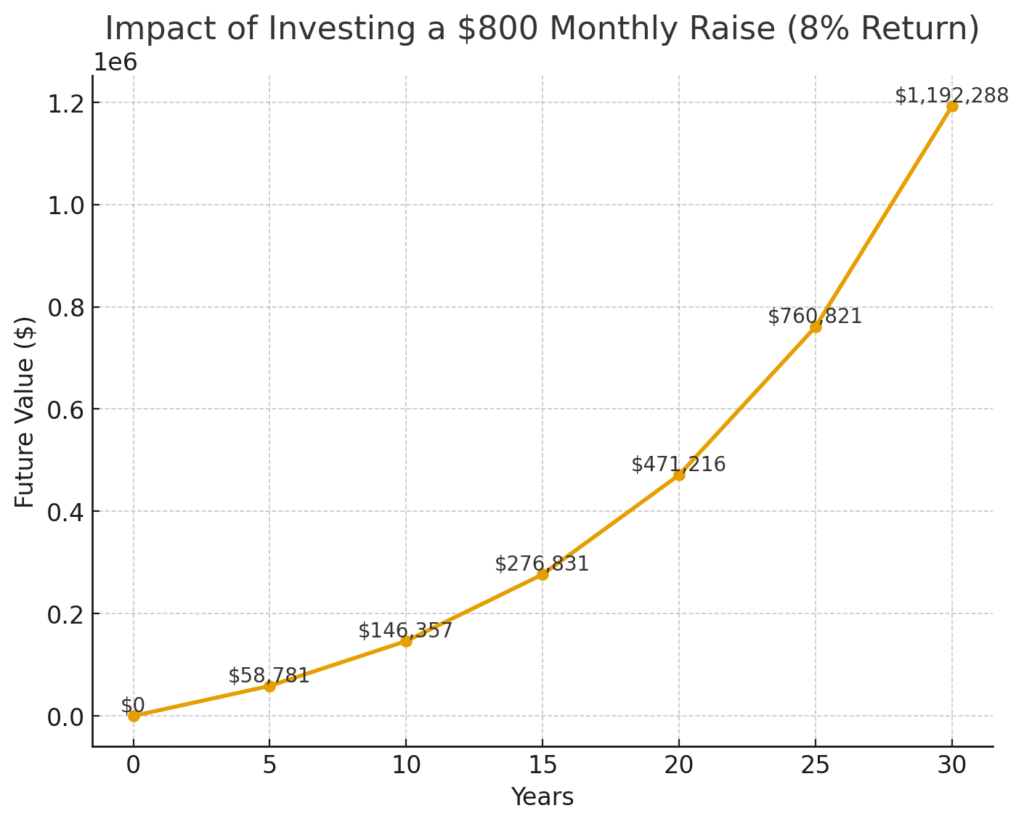

When your income rises, it’s tempting to upgrade your lifestyle. But instead of instantly spending your raise, imagine investing it.

For example, if you got a raise of $800/month and invested it into the S&P 500 at 8% return, look at the results:

📊 Chart: Impact of Investing a $800 Monthly Raise

- After 10 years → $145,000

- After 20 years → $440,000

- After 30 years → $1,065,000

💡 That raise could make you a millionaire if invested instead of spent.

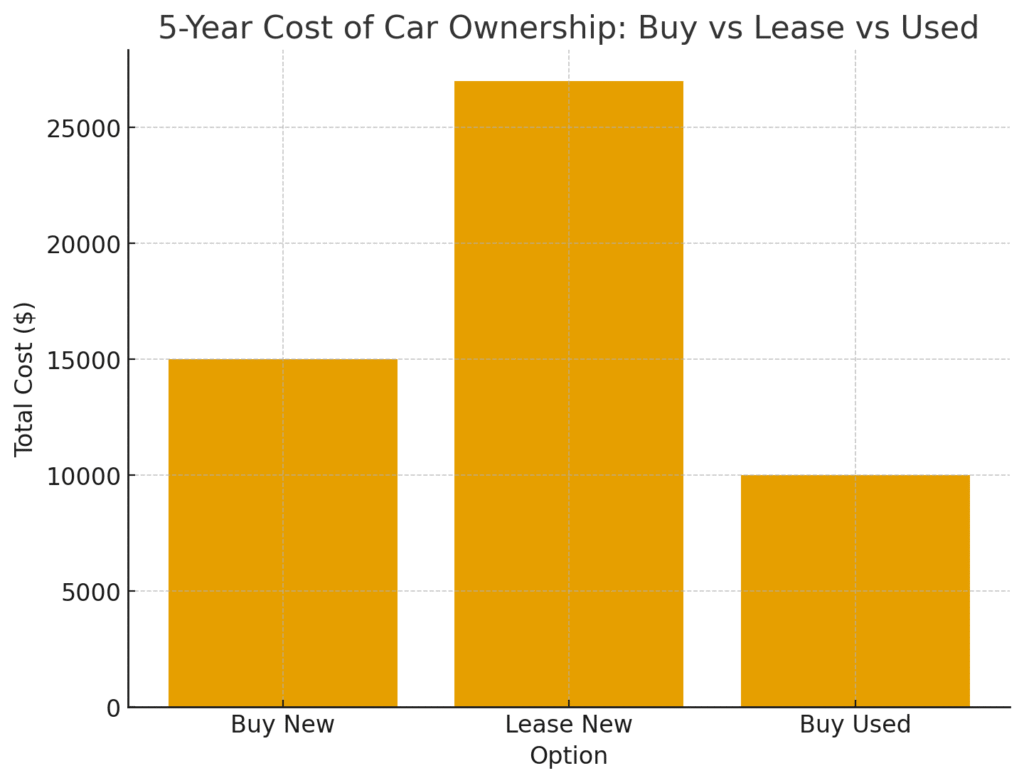

2. Cars as Wealth Killers

Cars are one of the fastest depreciating purchases you’ll ever make. Buying slightly used (3–5 years old) often saves thousands compared to leasing or buying new.

📊 Chart: 5-Year Cost of Car Ownership

- Buying New (5 years): $15,000 depreciation

- Leasing New (5 years): $27,000 paid, own nothing

- Buying Used (5 years): $10,000 depreciation

👉 Buying slightly used is usually the smartest choice. If you invested the difference (about $200/month saved vs leasing), in 10 years you’d have $36,000+ instead of losing money.

Therefore:

- Buy slightly used (3–5 years old).

- Avoid leasing unless you can easily afford the depreciation.

3. Emotional Spending

Impulse spending feels good in the moment but costs you big long-term.

Example: Buying $200 sneakers every 3 months = $800/year.

- Invested at 8% return → $39,000 after 20 years

- After 30 years → $100,000+

💡 That’s a luxury car or an early retirement fund hidden in your closet purchases.

Quick Fixes:

- Stick to a shopping list.

- Unsubscribe from marketing emails.

- Apply the 24-hour rule — delay purchases by a day.

Conclusion

Buying a house may feel like the ultimate financial milestone, but it’s not the only path to wealth. With the 65-25-10 rule, you can balance living well today and building security for tomorrow. By saving consistently, investing smartly, and avoiding money traps, you’ll unlock the ultimate financial goal: freedom.

You don’t need to be chained to a mortgage. You need a plan. And now, you have one.

Disclaimer

This blog post is for educational purposes only and does not constitute financial or investment advice. The information provided reflects general market data and personal opinion. Always do your own research or consult with a licensed financial advisor before making investment decisions.

FAQs

1. Is renting really better than buying?

Not always. But in many cities, renting + investing the difference beats owning, especially when mortgage + hidden costs are high.

2. How much should I invest each month?

Start with 10% of your net income. If that’s too high, start with what you can — even 2% builds the habit.

3. What if the stock market crashes?

Stay invested. Over 20+ years, markets recover and grow. The biggest returns come from time in the market, not timing the market.

4. Can I still buy a house one day?

Yes. The 65-25-10 rule doesn’t stop you from buying. It helps you do it without sacrificing your future wealth.

5. What’s the best first investment?

For beginners: low-cost index funds or employer retirement accounts with a company match.