Disclaimer: The information provided in this article is for educational and informational purposes only. It is not intended to be and should not be construed as professional tax, legal, or financial advice. Tax laws can change, and every individual’s financial situation is unique. Always consult with a qualified professional, such as a CPA or a financial advisor, for advice tailored to your personal circumstances.

Taxes in Canada keep going up, and for many Canadians, it feels harder each year to build wealth while a larger portion of their income goes to the government. It’s a common frustration, and a question many people ask is whether it’s even possible to get ahead. Fortunately, here’s the good news: with a strategic and thoughtful approach, you can legally and effectively reduce your tax burden in 2025 and, as a result, keep more of your hard-earned money.

This comprehensive guide is designed to empower you with knowledge. It will break down three proven, legal tax-saving strategies that every Canadian should know and actively consider:

- Maximizing Registered Accounts (RRSP, TFSA, FHSA)

- Switching from Employment Income to Business Income

- Using Real Estate to Build Wealth and Save on Taxes

Furthermore, to make these concepts concrete, we’ll use clear, illustrative examples, numbers, and descriptive charts so you can see the tangible difference these strategies can make.

Understanding Why Tax Planning Matters in Canada

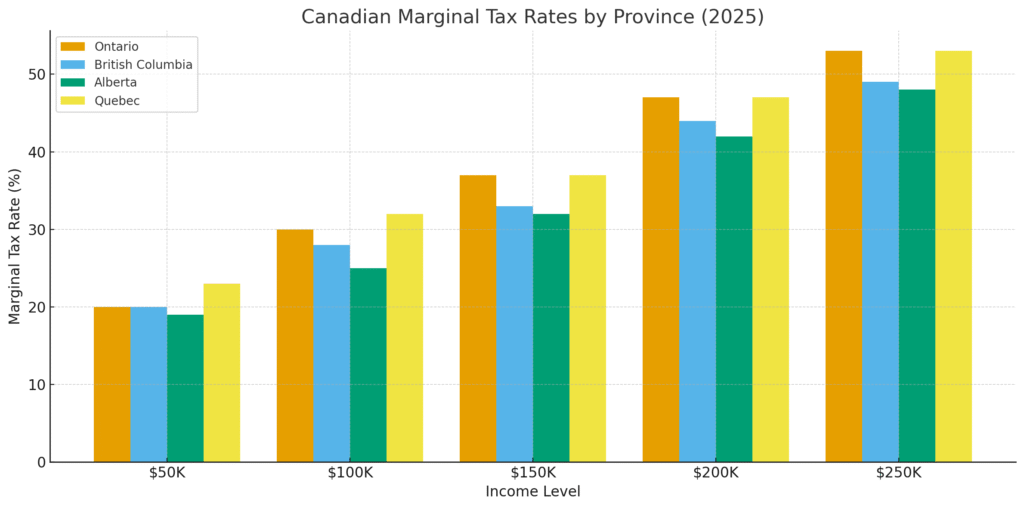

Before we dive into the specific strategies, it’s vital to grasp the core principle of tax planning. Canada’s tax system operates on a progressive scale. This means as your income increases, you get pushed into higher tax brackets where you pay a greater percentage of each additional dollar earned. This is your marginal tax rate, and for high-income earners in some provinces, it can indeed exceed 50%.

- This chart will visually represent the combined federal and provincial marginal tax rates for different income brackets across major Canadian provinces (e.g., Ontario, British Columbia, Alberta, Quebec) for the 2025 tax year. This helps readers immediately understand the impact of their income level.

Consequently, it’s not just about how much you earn—it’s about how much you keep. Think about it this way: if you can legally reduce your taxable income by $20,000, you aren’t just saving the taxes on that amount; you’re often saving them at your highest marginal tax rate. This is, in effect, giving yourself a significant raise without working any extra hours. Therefore, tax planning is not about avoiding your duty; it’s about playing by the rules of the system in the smartest way possible.

Strategy 1: Maximize Registered Accounts (RRSP, TFSA, FHSA)

For the majority of Canadians who are employees, registered accounts are one of the most accessible and powerful tools to legally reduce your taxable income and grow your wealth. These accounts are special because the government has created them specifically to encourage Canadians to save, and they come with significant tax advantages.

1. The RRSP: Your Tax-Deductible Powerhouse

The Registered Retirement Savings Plan (RRSP) is arguably the most well-known tax-saving tool for employees. Its primary benefit is that contributions are tax-deductible, which means they reduce your taxable income for the year you make them. In addition, the investments inside your RRSP grow tax-deferred, meaning you don’t pay any tax on the investment gains until you eventually withdraw the money, typically in retirement.

- Who Should Use It? An RRSP is especially powerful if you are currently in a high tax bracket and expect to be in a lower one during retirement. The tax deduction today provides an immediate refund or reduces your tax payable, and you get to benefit from tax-deferred compounding for years or even decades.

- Contribution Rules: The 2025 RRSP contribution limit is 18% of your earned income from the previous year, up to a maximum of $32,490. Unused contribution room can be carried forward, so you don’t lose it.

- Hypothetical Example:

- Case: Sarah is a project manager in Ontario with a gross income of $100,000. Her combined federal and provincial marginal tax rate is approximately 30%.

- Action: She contributes $18,000 to her RRSP, an amount equal to her 18% limit.

- Result: Her taxable income drops to $82,000. Her tax savings are approximately $5,400 ($18,000 x 30%). She gets a nice refund on her tax return that she can reinvest or use for other financial goals.

2. The TFSA: Your Tax-Free Wealth Builder

In contrast to the RRSP, the Tax-Free Savings Account (TFSA) doesn’t give you an upfront tax deduction. Instead, its magic lies in its tax-free growth. All investment gains—be it from stocks, ETFs, mutual funds, or GICs—and all withdrawals are 100% tax-free, forever.

- Who Should Use It? A TFSA is ideal for both short-term and long-term goals. It’s particularly useful for those in lower tax brackets who want to save for a major purchase without worrying about future taxes. The tax-free withdrawals also make it a great tool for a retirement nest egg that won’t affect your government benefits like Old Age Security (OAS).

- Contribution Rules: The 2025 TFSA contribution limit is $7,000. This limit is in addition to any unused contribution room from previous years.

- Hypothetical Example:

- Case: Mark invests $7,000 every year into his TFSA for 30 years and earns a conservative 8% average annual return.

- Action: He contributes for 30 years, totaling $210,000.

- Result: The value of his TFSA could grow to over $880,000, with every single penny of that money being 100% tax-free upon withdrawal.

3. The FHSA: The Hybrid Home Saver

The First Home Savings Account (FHSA) is a relatively new account, but it’s a game-changer for prospective first-time homebuyers. It uniquely combines the best features of both the RRSP and the TFSA.

- Contribution Rules: The 2025 FHSA contribution limit is $8,000 per year, with a $40,000 lifetime limit. Unused room can be carried forward, but only for a single year.

- Key Benefits: Contributions are tax-deductible, reducing your current-year taxable income, just like an RRSP. Furthermore, withdrawals for the purpose of buying a first home are entirely tax-free, just like a TFSA. This dual benefit makes it a powerful tool for accelerating your home-buying timeline.

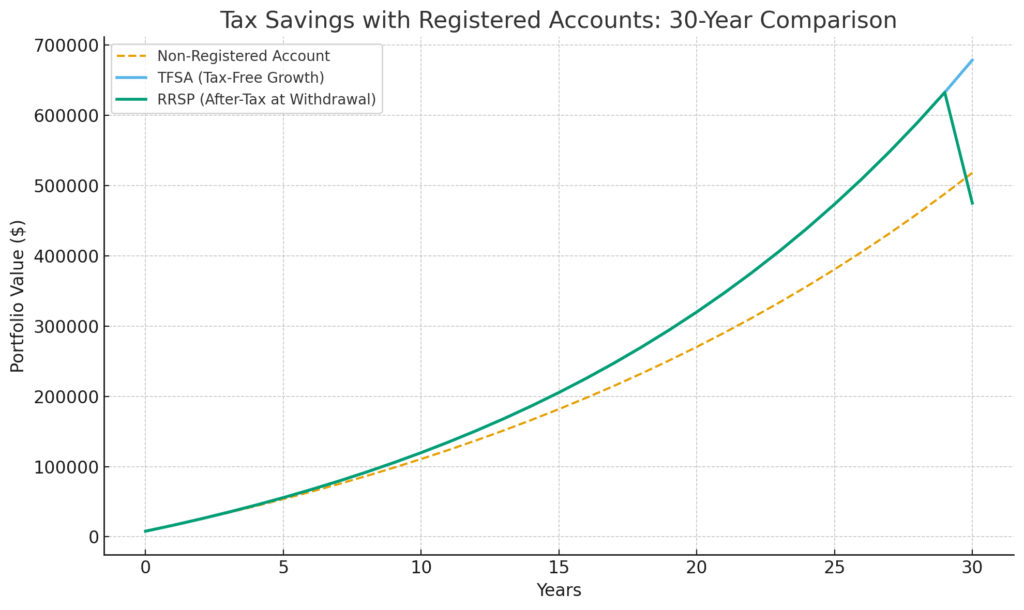

- This chart would show a comparison of three investment scenarios over 30 years: a non-registered account, a TFSA, and an RRSP. It will clearly illustrate how a TFSA’s tax-free growth and an RRSP’s tax deferral can lead to significantly more wealth than a regular taxable account.

Strategy 2: Switching from Employment Income to Business Income

For many Canadians, employment income is the simplest and most common form of income. However, from a tax perspective, it is the least flexible. The biggest financial lesson many successful individuals learn is the power of switching from employment income to business income.

- As an employee, you are taxed on 100% of your salary. Your deductions are limited almost exclusively to RRSP contributions and a few minor credits.

- As a business owner, you gain a new level of control. You can deduct eligible business expenses before your income is even taxed. Furthermore, you can choose to incorporate your business and pay lower corporate tax rates (which can be as low as 9-12% on the first $500,000 of active business income in many provinces), rather than the much higher personal tax rates.

Types of Tax-Deductible Business Expenses

This is where the magic truly happens. A business owner can deduct a wide array of legitimate expenses that are directly related to generating income. This includes:

- Home Office Expenses: A portion of your rent/mortgage interest, utilities (hydro, gas, internet), property taxes, and home insurance.

- Motor Vehicle Expenses: The cost of gas, insurance, repairs, and maintenance for a vehicle used for business purposes.

- Professional Fees: Fees for accountants, lawyers, and business consultants.

- Office Supplies and Equipment: Computers, software subscriptions, stationery, and other materials.

- Travel and Meal Expenses: A portion of the cost of meals, hotels, and transportation for business-related travel.

- Advertising and Marketing: The cost of building a website, running ads, or creating a brand.

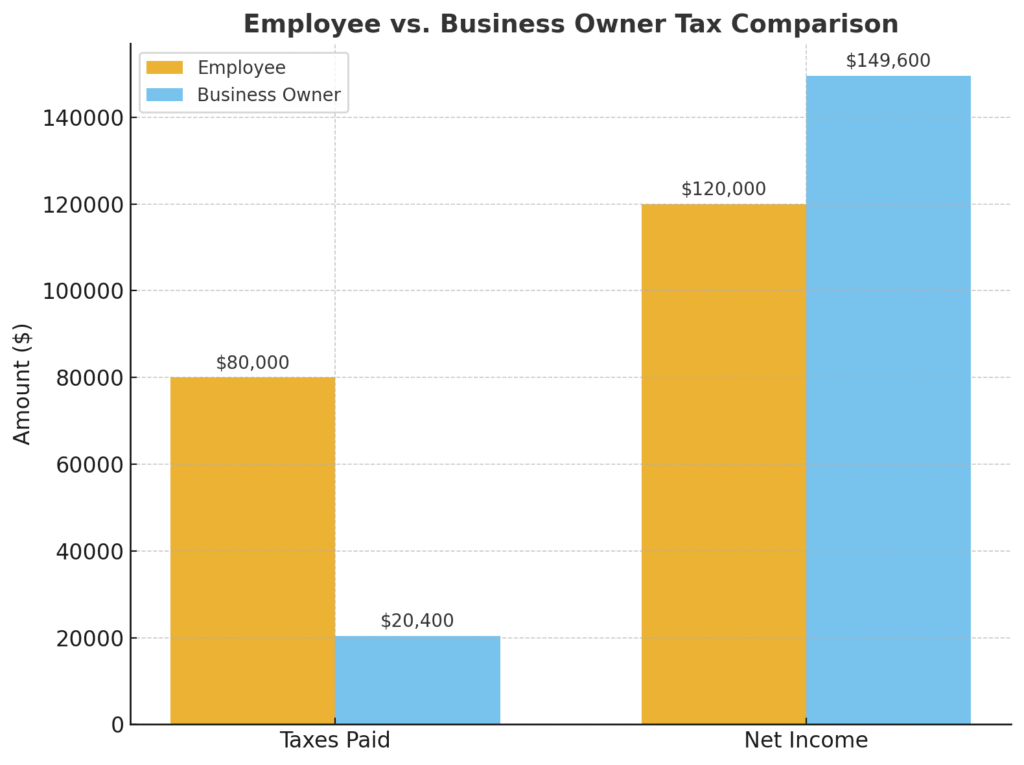

Hypothetical Case Study: The Employee vs. The Business Owner

Let’s examine a hypothetical case to see the significant tax difference between an employee and a business owner.

- Case 1: The Employee

- Salary: $200,000

- Taxable Income: $200,000

- Taxes Paid: Approximately $80,000 (assuming a simplified 40% combined tax rate)

- Net Income: $120,000

- Case 2: The Business Owner

- Gross Revenue: $200,000

- Legitimate Business Expenses: $30,000 (home office, car expenses, software, etc.)

- Taxable Business Income: $170,000

- Taxes Paid: If incorporated, this income could be taxed at a small business tax rate of around 12% on the first portion, which is approximately $20,400.

- Net Retained Earnings in the corporation: $149,600

As you can clearly see, that’s a difference of nearly $30,000 saved in taxes every single year. This is a powerful illustration of the tax efficiency that a business structure can provide.

- This graph would visually contrast the tax burden of a high-income employee versus a high-revenue business owner after deducting eligible expenses and applying a lower corporate tax rate. It would make the difference in net income very clear.

Strategy 3: Using Real Estate for Tax Savings and Wealth

Real estate in Canada is often seen as a key to wealth, and for good reason. It’s not just about a home; it’s a versatile asset that offers multiple channels for tax savings and wealth accumulation.

1. The Principal Residence Exemption

This is one of the most powerful tax exemptions available to Canadians. If you sell your primary residence, you don’t pay any capital gains tax on the profit from the sale.

- Rules to Know:

- The property must have been your primary residence for every year you owned it.

- If you have a home office, a small portion of the home’s value may not qualify for the exemption if you have a dedicated business space and have made structural changes to the home for business use.

- You can only designate one property as your principal residence per family unit per year.

- Illustrative Example:

- Case: You bought a condo for $500,000 in 2015 and sold it for $1,000,000 in 2025.

- Result: The profit (capital gain) is $500,000. Because it was your principal residence, your taxes owed on that gain are $0.

2. Rental Properties: Tax Deductions and Wealth Building

Owning a rental property allows you to use legitimate expenses to reduce the taxable income you earn from rent.

- Common Deductible Expenses:

- Mortgage interest

- Property taxes

- Home insurance

- Maintenance and minor repairs

- Utilities (if included in rent)

- Professional fees (property management, accounting, legal fees)

- Advertising for tenants

- The Power of Depreciation (Capital Cost Allowance): You can also deduct a portion of the value of your rental property’s building over time, known as Capital Cost Allowance (CCA). This can further reduce your taxable income, although there are complexities to this strategy and a “recapture” of the tax benefit when the property is sold.

- Illustrative Example:

- Case: You own a rental property that generates $24,000 in annual rental income. Your expenses (mortgage interest, property tax, maintenance, etc.) total $15,000 per year.

- Result: Your taxable rental income is only $9,000 ($24,000 – $15,000). You are building wealth through appreciation and equity growth, but you are only paying tax on a fraction of the income.

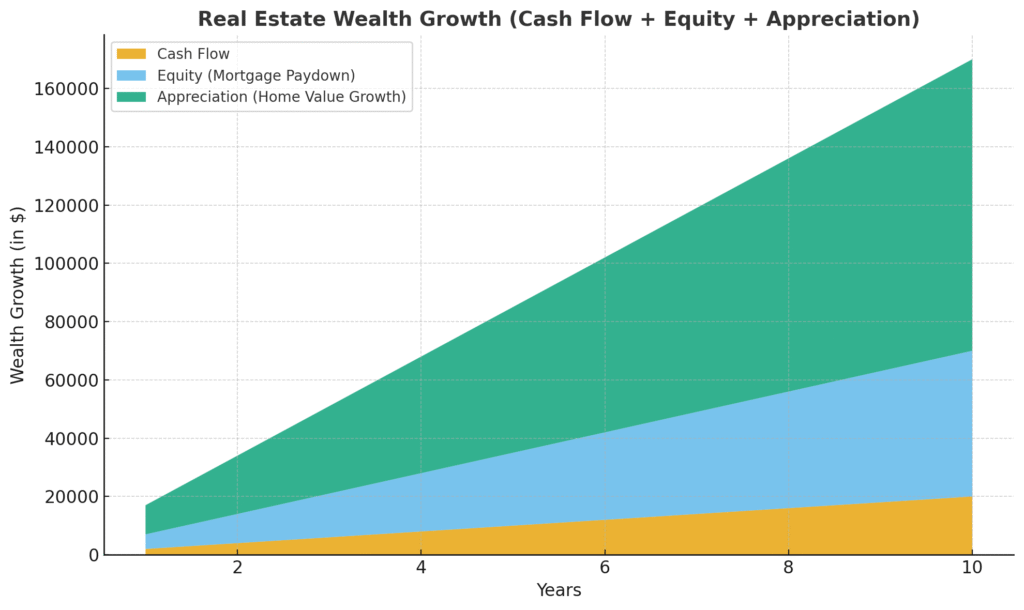

Here’s the chart showing Real Estate Wealth Growth broken down into Cash Flow, Equity (Mortgage Paydown), and Appreciation (Home Value Growth) over 10 years.

Hypothetical Case Study: The Doctor Who Changed His Tax Strategy

I once heard of a doctor in Canada earning over $250,000 per year, yet he was living paycheck-to-paycheck. Why? He relied solely on employment income, had no registered accounts, no business structure, and no rental properties. His entire salary was being taxed at the highest possible marginal rates.

After a financial advisor introduced him to these concepts, he shifted his strategies dramatically:

- He incorporated his medical practice, which allowed him to pay himself a salary and use retained earnings for investments, benefiting from a lower corporate tax rate.

- He opened an RRSP and a TFSA, maxing them out to reduce his personal taxable income and begin building a tax-free nest egg.

- He bought a rental condo, allowing him to deduct expenses and build wealth in the background.

Within just three years, he went from feeling financially stressed to building significant long-term wealth. His mindset shifted from “how much can I earn?” to “how much can I keep and invest?”

Final Thoughts: Your Action Plan

Learning how to pay less taxes in Canada in 2025 isn’t just about the numbers; it’s about a change in mindset. It’s a shift from being a passive taxpayer to an active tax planner.

Your journey starts here. Whether you are a full-time employee, a self-employed professional, or a budding investor, you now have the knowledge to take control of your financial future.

- As an employee, your immediate action plan should be to prioritize and maximize your contributions to your RRSP, TFSA, and FHSA.

- For business owners, it’s about diligently tracking all eligible expenses and strategically planning for the future, including considering incorporation.

- As an investor, the goal is to use tax-efficient investment vehicles like real estate to grow your wealth while minimizing your tax burden.

Remember, the goal isn’t just to make a living; it’s to build a legacy. And to do that, you must master the art of how much you keep.

Frequently Asked Questions About Paying Less Taxes in Canada

Q1: Is it legal to pay less taxes in Canada?

Yes, absolutely. The strategies discussed in this article, and many others, are 100% legal. The Canada Revenue Agency (CRA) provides these accounts and deductions to encourage Canadians to save for retirement, buy homes, and create jobs through small businesses. Tax planning is not about tax evasion; it’s about using the rules of the system to your advantage, which is a fundamental part of financial responsibility.

Q2: Should I max out my RRSP or TFSA first?

This is one of the most common questions in Canadian finance, and the answer depends on your specific situation. As a general rule, if you are currently in a high tax bracket and believe you will be in a lower one in retirement, an RRSP often provides the most value due to the large upfront tax deduction. Conversely, if you are in a lower tax bracket or saving for a shorter-term goal, the TFSA’s tax-free growth and withdrawals can be more beneficial.

Q3: Do I need to incorporate to save on taxes?

Not always. For many small-scale freelancers or consultants, a sole proprietorship is simpler to manage. However, once your self-employment income is consistent and exceeds roughly $100,000 per year, the tax advantages of incorporating, particularly the ability to access a lower tax rate and defer personal income tax, can become significant.

Q4: Can I deduct my home office even if I’m not incorporated?

Yes. If you are a self-employed individual, you can claim a portion of your home expenses as a tax deduction if your home is your principal place of business or is used exclusively for earning business income on a regular and ongoing basis.

Q5: Is real estate still worth it with new tax rules?

Yes, for most investors, it is. While the government has introduced new rules like the anti-flipping tax, the fundamental tax benefits of holding rental properties (deducting expenses) and the Principal Residence Exemption for a primary home remain powerful tools for building wealth.