Introduction: Why Inflation Is Quietly Draining Your Wealth

Imagine this: a few years ago, you could walk into Starbucks and grab a caramel frappuccino for $5. Fast forward to today, and that same drink is closer to $8 or even $9. That’s not because Starbucks suddenly decided to make it more luxurious — it’s inflation.

Inflation is the slow, steady rise in prices over time. While it may not seem like a big deal year to year, it eats away at your money’s value. What cost you $50 for groceries five years ago might now cost $75 or more.

Here’s the hard truth: if your money is sitting in a savings account earning 1% interest while inflation is at 3–4%, you’re losing money without even spending it. That $1,000 you’ve worked hard to save will buy less next year than it does today.

But here’s the good news — you don’t have to just watch your money shrink. You can fight back by investing. Investing makes your money work for you so that it grows faster than inflation. This guide will break it down step by step, in plain English, with real-world examples.

By the end of this article, you’ll know:

- Why investing is more powerful than saving.

- Which investments make sense for beginners.

- How much you should start with.

- A simple example of buying your first stock or ETF.

- How to stay calm when the market goes down.

Let’s dive in.

Part 1: Why Invest Instead of Save?

Saving feels safe. You put your money in a savings account, and you know it’s “there.” The problem? Safety doesn’t mean growth.

Let’s do some quick math.

👉 Suppose you have $10,000 in a savings account earning 1% interest. In a year, you’ll have $10,100.

But if inflation is 3%, the cost of goods that used to be $10,000 will now be $10,300. That means even though you earned $100 in interest, you actually lost $200 in buying power.

This is why so many people feel like they’re working harder but not getting ahead — because their savings aren’t keeping up with rising costs.

Now, compare that to investing.

If you took that same $10,000 and put it in an S&P 500 index fund (which historically returns 7–10% a year on average), in one year you might have around $10,700 to $11,000.

Not only does this beat inflation, but it grows your money over time thanks to compound interest.

The Snowball Effect of Compounding

Albert Einstein famously called compound interest the “eighth wonder of the world.” Why? Because it’s money that makes money, which then makes even more money.

Here’s an example:

- If you invest $500 a month at 10% annual growth:

- After 10 years → about $95,000

- After 20 years → about $315,000

- After 30 years → nearly $1 million

Notice how the curve speeds up? That’s the snowball effect in action. The earlier you start, the bigger the snowball becomes.

Part 2: What Should Beginners Invest In?

If you’re new to investing, you might feel overwhelmed. Stocks, bonds, crypto, real estate — where do you even start?

Here’s the truth: most beginners lose money because they chase trends. They hear about a stock that doubled last year and rush to buy, only to watch it crash. Remember Blackberry? At its peak, shares were over $145. Today, it’s a fraction of that.

So, what’s safer and smarter? Index funds and ETFs.

Why Index Funds and ETFs Work

- Diversification: Instead of betting on one company, you’re investing in hundreds at once.

- Lower risk: If one company struggles, the others balance it out.

- Simplicity: You don’t need to be a stock-picking genius.

- Proven growth: The S&P 500 has returned about 10% annually over the long term.

Example: The S&P 500 ETF (SPY)

If you bought $1,000 of SPY (an S&P 500 ETF) in 2010, it would be worth over $4,500 today (2025). And that’s without you doing anything fancy — just holding and waiting.

Other popular beginner-friendly ETFs include:

- VOO – Vanguard’s S&P 500 ETF.

- QQQ – Tracks top technology companies like Apple, Microsoft, and Nvidia.

- SPLG – A low-cost S&P 500 ETF.

👉 Pro Tip: Check the expense ratio before buying. If an ETF has an expense ratio of 0.03%, it means you pay just $3 per year for every $10,000 invested.

Part 3: When and How Much Should You Invest?

The best time to start investing? Now.

But before you do, ask yourself two questions:

- Do I have high-interest debt (like credit card debt)?

- If yes, pay that off first. Paying off a credit card with 20% interest is like getting a guaranteed 20% return.

- Example: If you have $10,000 debt at 25% interest, you’re losing $2,500 a year. Paying that off is smarter than investing.

- Do I have an emergency fund (3–6 months of expenses)?

- Life happens — car breakdowns, job loss, medical bills. Having a cushion prevents you from selling investments at the worst time.

Once you’ve covered those, you’re ready.

How Much Should You Invest?

You don’t need thousands of dollars to begin. Many apps let you start with just $1. But the more consistent you are, the faster you’ll see results.

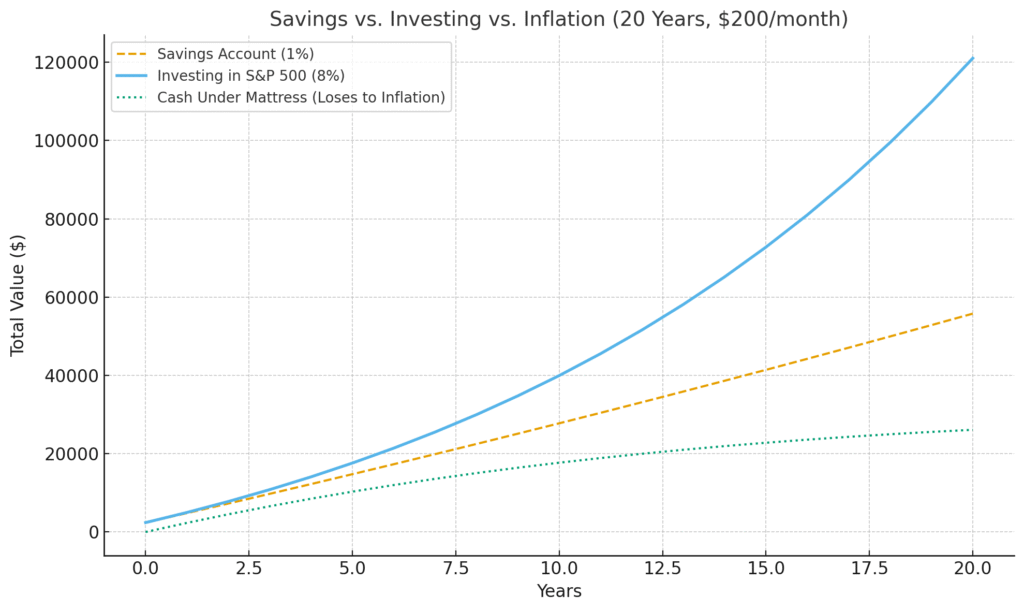

👉 Example: If you invest $200/month at 8% growth:

- 10 years → about $36,000

- 20 years → about $120,000

- 30 years → about $300,000

It’s not about timing the market perfectly — it’s about time in the market.

Here’s a clear visual comparison showing how $200/month grows over 20 years:

- Savings account (1%) → grows slowly, barely keeping up.

- Cash under the mattress → loses value every year due to inflation.

- Investing in S&P 500 (8%) → skyrockets, showing the real power of compounding.

Part 4: Step-by-Step Example of Buying Your First ETF

Let’s make this super practical. Say you want to buy shares of SCHD, a dividend-focused ETF.

- Open a brokerage account (Vanguard, Fidelity, Charles Schwab, or Robinhood).

- Deposit funds from your bank account.

- Search the ticker symbol (SCHD).

- Click “Buy” → Enter the number of shares (or dollar amount if fractional shares).

- Choose “Market Order” for simplicity.

- Confirm your purchase.

Congratulations — you’re now an investor. 🎉

Part 5: Long-Term Investing Strategies

Here’s the biggest secret of successful investors: they don’t panic.

Markets go up and down like a roller coaster, but over time, they trend upward.

Example: The 2008 Financial Crisis

- If you bought SPY in 2007 at $154/share, it crashed to $73 in 2009. Many sold in fear.

- But if you held on, by 2025 SPY is around $500–$600/share. That’s nearly a 4x return.

Selling in panic locks in losses. Holding with patience rewards you.

Golden Rules for Beginners

- Invest for at least 5–10 years.

- Automate monthly contributions (dollar-cost averaging).

- Ignore the noise in the media.

- Don’t try to “time the market.”

The following are illustrative examples of how consistent investing can lead to significant wealth. While these stories are not of real individuals, the results are based on realistic market returns over time.

1. Sarah – The Teacher Who Turned $200 a Month into Six Figures

Sarah, a high school teacher, always thought investing was only for “Wall Street people.” But when she realized her savings account was barely keeping up with rising grocery bills, she decided to give investing a shot.

She started small: $200 a month into an S&P 500 index fund (VOO).

- After 10 years, her account had grown to about $36,000.

- After 20 years, it grew to around $120,000.

- Today, 25 years later, Sarah’s portfolio is worth nearly $200,000 — all from slow, steady investing.

Her secret wasn’t timing the market or chasing the latest hot stock. It was simply consistency. Even when the market dipped, she kept buying, and those dips turned into opportunities.

Sarah often says:

“I never missed the money because I treated investing like a bill I had to pay. The difference is, this bill pays me back.”

2. James – The Young Professional Who Started Early

James got his first job at 22, earning $45,000 a year. Instead of upgrading his car or spending big on nights out, he committed to investing $500 a month in a mix of ETFs (VOO and QQQ).

By age 32, just 10 years later, James had over $95,000 invested.

Now at 40, his account is valued at more than $315,000, and he’s on track to become a millionaire in his 50s — not because of a high-paying job, but because he gave his money time to grow.

His friends used to tease him for being “cheap,” but now they’re asking him for investing advice.

3. Maria and David – Parents Who Secured Their Kids’ College Fund

Maria and David were worried about rising education costs. They didn’t want their two kids to graduate with crushing student loans. So instead of just saving, they invested $250 a month per child into a broad-market ETF.

By the time their oldest turned 18, their investments had grown to about $90,000. That was enough to cover tuition at a state university without debt.

For them, investing wasn’t about getting rich — it was about giving their kids a future without financial stress.

4. Mark – The Guy Who Panicked and Learned the Hard Way

Not every story is rosy. Mark invested $20,000 in 2007, right before the 2008 financial crisis. When his account dropped by half, he panicked and sold everything at a loss.

If Mark had just held on, his original $20,000 investment would be worth around $80,000 today.

He learned the hard way that the biggest mistake beginners make is panic-selling. Now, Mark invests regularly and refuses to check his account every day.

His advice?

“Your emotions are your worst enemy. Once I stopped panicking and trusted the process, my money started working for me.”

The Takeaway

These stories prove that you don’t need to be wealthy or a financial expert to grow your money. You just need three things:

- Start as soon as possible.

- Be consistent (even small amounts add up).

- Don’t panic when the market dips.

If Sarah the teacher, James the young professional, and Maria & David the parents can do it, so can you.

Conclusion: Don’t Let Inflation Win

Inflation is inevitable, but being unprepared isn’t. Every dollar you leave idle loses buying power over time. Investing is your best defense.

The earlier you start, the more powerful compounding works in your favor. Whether you begin with $50 or $500 a month, consistency is the key to building wealth and protecting your future.

So ask yourself: will you let inflation eat away at your money, or will you put your money to work and grow your wealth?

The choice is yours.

Disclaimer

This blog post is for educational purposes only and does not constitute financial or investment advice. The information provided reflects general market data and personal opinion. Always do your own research or consult with a licensed financial advisor before making investment decisions.

FAQs About Inflation and Investing

Q1: Can savings accounts beat inflation?

Not really. Most savings accounts earn less than 2%, while inflation averages 3–4%.

Q2: What’s the safest way to start investing?

Index funds and ETFs tracking the S&P 500 are considered the most reliable for beginners.

Q3: How much money should I start with?

Even $1 gets you started. But aiming for $100–$500/month builds serious momentum.

Q4: Should I invest if I still have debt?

Pay off high-interest debt first. Then invest.

Q5: How long should I hold my investments?

At least 5 years — ideally decades. Compounding rewards patience.