Imagine two friends, Sarah and John.

Sarah started investing in low-cost index funds 15 years ago. She didn’t stress over the stock market daily, didn’t chase “hot picks,” and simply let her investments grow. Today, she has nearly $200,000 in her retirement account—without ever trying to “beat the market.”

John, on the other hand, jumped from one actively managed mutual fund to another. He paid high fees, trusted fund managers who promised “market-beating returns,” and even tried a hedge fund his uncle recommended. Today, he has far less than Sarah—even though he invested the same amount.

👉 This isn’t just a story about two people. It’s the reality of investing choices. The type of fund you choose—index fund, mutual fund, hedge fund, or ETF—can make a massive difference in your long-term wealth.

If you’ve ever wondered:

- What’s the difference between these funds?

- Which one actually makes me the most money?

- Which one is safest for beginners?

…then you’re in the right place. This guide will break everything down with examples, comparisons, charts, and FAQs, so you’ll walk away with clarity and confidence.

Let’s dive in.

What is a Fund? (The Birthday Party Analogy)

At its core, a fund is just a pool of money.

Imagine you and five friends want to throw a big birthday bash. Instead of one person paying for everything, everyone chips in. With that pooled budget, you can afford a bigger cake, better music, and more decorations than if each person threw a party alone.

A fund works the same way:

- Investors pool their money together.

- That money is invested in a basket of assets (stocks, bonds, real estate, commodities, etc.).

- Everyone shares in the profits (or losses) based on how much they contributed.

👉 The benefit? Diversification, professional management, and lower risk compared to picking individual stocks on your own.

But here’s where it gets tricky: Not all funds are the same. Some are cheap and beginner-friendly. Others are expensive, risky, and only for the ultra-rich.

The four most common types you’ll hear about are:

- Index Funds

- Mutual Funds

- Hedge Funds

- ETFs (Exchange-Traded Funds)

Let’s break them down one by one.

Index Funds: The Low-Cost Wealth Builder

Index funds are the darling of personal finance experts—and for good reason.

Instead of trying to “beat the market,” index funds simply mirror an index. For example:

- The S&P 500 index tracks the 500 largest U.S. companies.

- The NASDAQ tracks tech-heavy giants like Apple, Amazon, and Microsoft.

- The Dow Jones tracks 30 large industrial companies.

Why People Love Index Funds

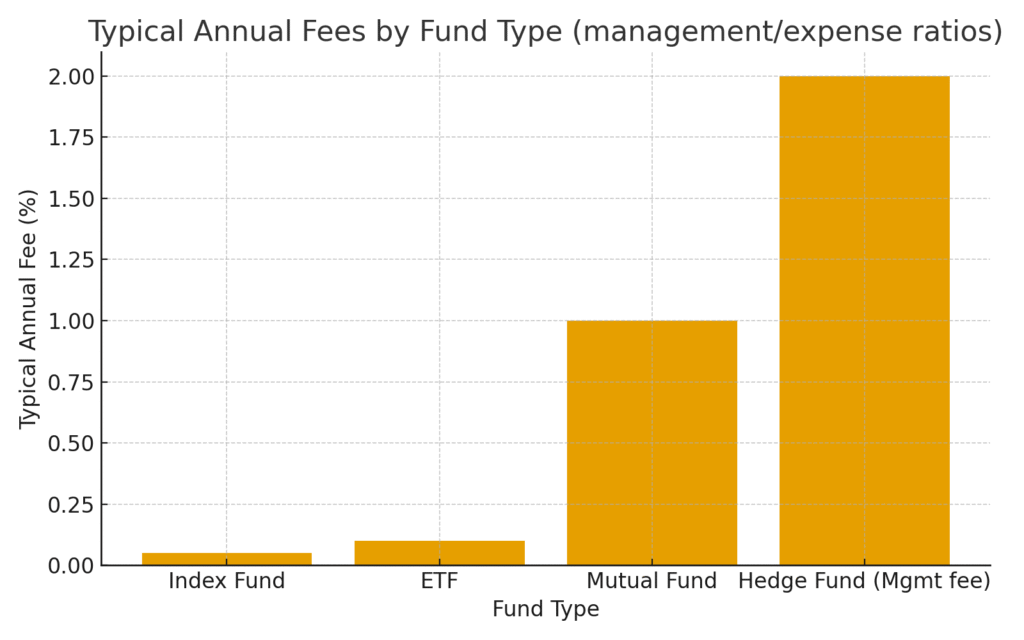

- Low Fees → No expensive managers. Typical expense ratio: 0.02%–0.20%.

- Diversification → One investment = hundreds of companies.

- Simplicity → No stock-picking stress.

- Long-Term Growth → Historically, the S&P 500 has returned ~10% annually.

Example

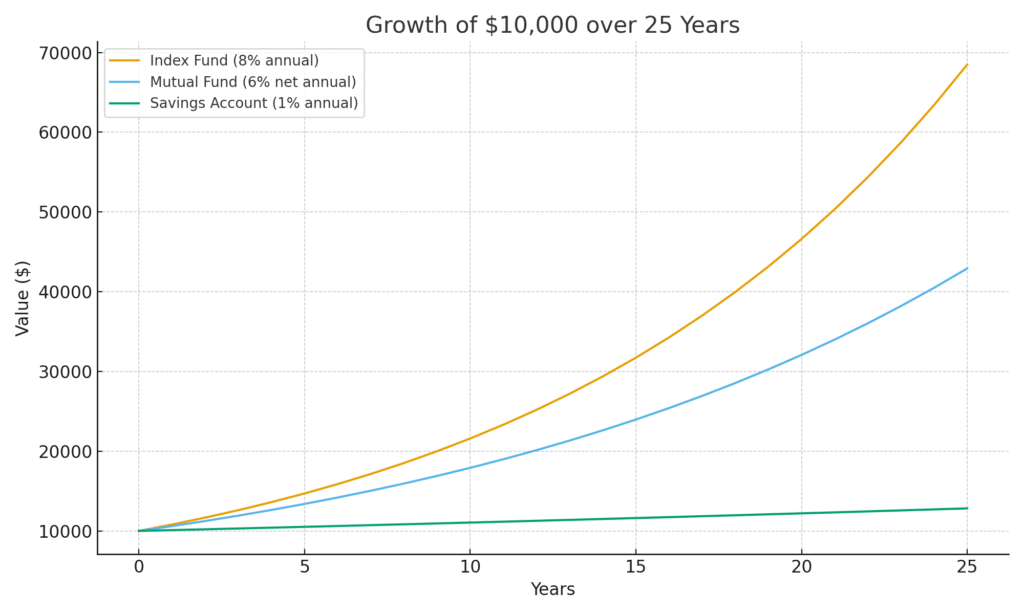

If you invested $10,000 in an S&P 500 index fund in 2000, you’d have over $60,000 today. If instead, you kept it in a savings account at 1% interest, you’d have only $12,200.

📊 (Chart: “$10,000 invested in S&P 500 vs Savings Account: 2000–2025”)

Downsides

- Trades only once per day (at NAV).

- No chance to outperform the market—only track it.

👉 Best For: Beginners, long-term investors, and anyone who wants “set it and forget it” investing.

Mutual Funds: Managed by Professionals (At a Cost)

Mutual funds are often confused with index funds, but here’s the key difference:

- Index funds = follow the market.

- Mutual funds = try to beat the market.

Features of Mutual Funds

- Active management → Fund managers buy/sell to maximize returns.

- Higher fees → Expense ratios often 0.5%–1.5% (some even higher).

- Diversification → Like index funds, they spread risk across many assets.

- End-of-day trading only → You buy/sell at NAV, calculated after markets close.

Example

Let’s say you invest in a mutual fund focused on tech stocks. If the fund manager thinks Tesla will skyrocket, they’ll buy more. If Apple seems weak, they might sell it off.

Sometimes they’re right. Sometimes not.

Here’s the kicker: Over 80% of actively managed funds fail to beat index funds in the long run (after fees).

📊 (Chart: “Average Fees: Index Funds vs Mutual Funds”)

Downsides

- High fees eat into returns.

- Many don’t outperform the market.

👉 Best For: Investors who strongly believe in a manager’s strategy or want exposure to niche sectors not available in index funds.

Hedge Funds: High Risk, High Reward

When you hear “hedge fund,” you might picture Wall Street billionaires—and you’re not far off.

Features of Hedge Funds

- Exclusive access → Usually limited to accredited investors (net worth $1M+).

- Aggressive strategies → Short-selling, leverage, derivatives.

- High fees → Famous “2 and 20” model (2% of assets + 20% of profits).

- Potential for extreme gains…or extreme losses.

Example

- In 2008, hedge fund manager John Paulson made $20 billion betting against the housing market.

- At the same time, other hedge funds collapsed completely.

⚠️ For everyday investors, hedge funds are too risky, too expensive, and out of reach.

👉 Best For: Ultra-wealthy investors who can afford high risk and want complex strategies.

ETFs: Flexible and Popular

ETFs (Exchange-Traded Funds) are often described as a hybrid between stocks and funds.

Features of ETFs

- Trade like stocks → You can buy/sell anytime during the trading day.

- Diversification → Like index funds, they can hold hundreds of assets.

- Low fees → 0.03%–0.75% on average.

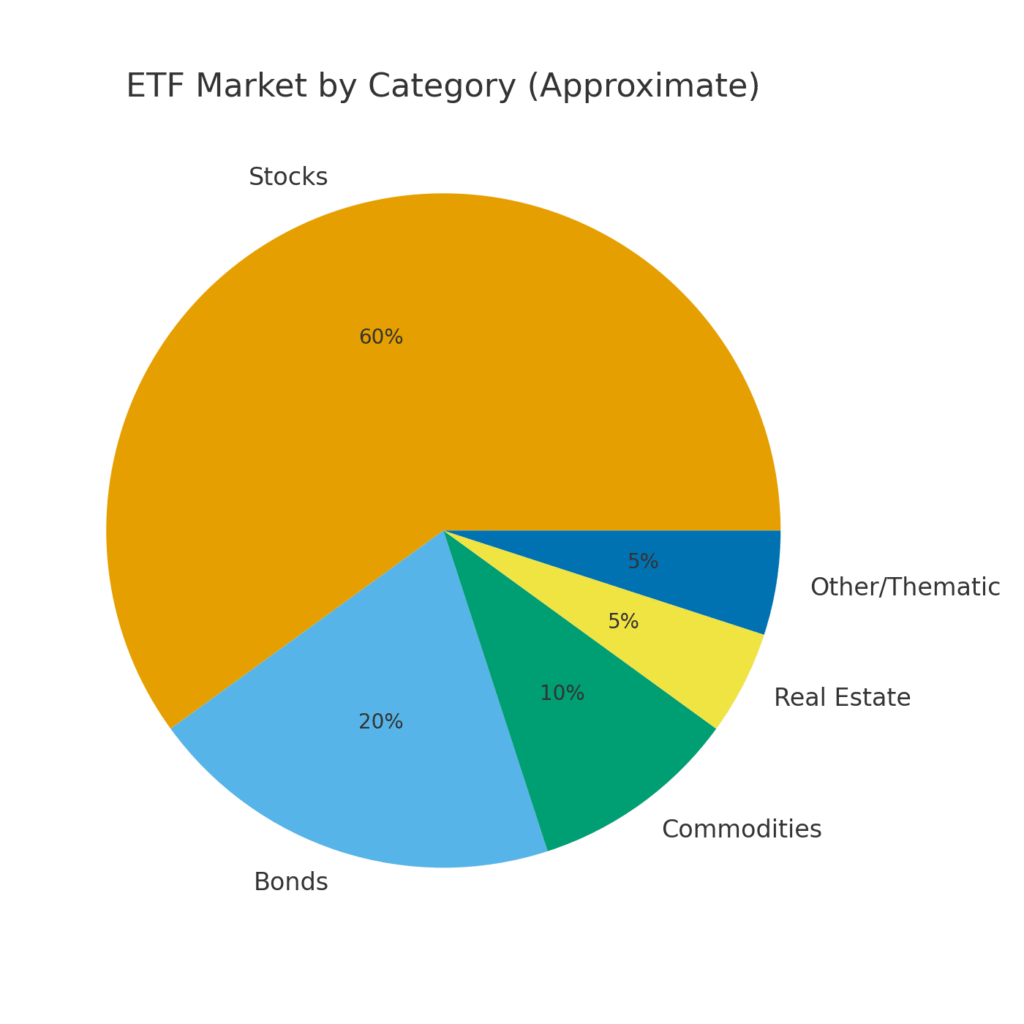

- Variety → ETFs exist for almost anything: S&P 500, gold, bonds, real estate, even Bitcoin.

Example

Instead of buying physical gold, you can buy the SPDR Gold ETF (GLD), which tracks gold prices. No vault required.

📊 (Chart: “Types of ETFs by Category: Stocks, Bonds, Commodities, Others”)

Downsides

- Brokerage fees (though many platforms now offer commission-free ETFs).

- Can be confusing because there are so many types.

👉 Best For: Investors who want flexibility, real-time pricing, and exposure to specific sectors or themes.

Side-by-Side Comparison

| Feature | Index Funds | Mutual Funds | Hedge Funds | ETFs |

|---|---|---|---|---|

| Management Style | Passive | Active | Aggressive | Passive/Active |

| Fees (avg) | 0.02–0.20% | 0.5–1.5% | 2% + 20% | 0.03–0.75% |

| Accessibility | Anyone | Anyone | Accredited | Anyone |

| Risk Level | Low-Medium | Medium | High | Low-Medium |

| Liquidity | End of day | End of day | Limited | Intraday |

| Best For | Beginners, long-term | Active belief | Wealthy elite | Flexibility |

Conclusion: Which One Should You Choose?

- Index Funds → Best for beginners and long-term investors.

- ETFs → Best for flexibility and real-time trading.

- Mutual Funds → Best if you believe in an active manager’s strategy.

- Hedge Funds → Best only for the ultra-rich with high risk tolerance.

At the end of the day, your choice depends on your goals, timeline, and risk tolerance. But for most people, index funds and ETFs remain the smartest, most cost-effective way to build wealth.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial advice. Investing involves risk, including the potential loss of principal. Always consult with a qualified financial professional before making any investment decisions.

FAQs

1. Which is better: index funds or ETFs?

Both are great. ETFs trade like stocks (real-time), while index funds are simpler for long-term investors.

2. Are mutual funds outdated?

Not necessarily. They still have a place, but most underperform index funds after fees.

3. Can hedge funds make me rich?

Possibly, but they’re risky, expensive, and not accessible to most investors.

4. What’s the safest investment fund?

Broad-market index funds or ETFs, because of diversification and low costs.

5. Can I lose money in an index fund?

Yes, in the short term. But historically, long-term investors have seen strong returns.