Why Wealth Building Feels Complicated (But Isn’t)

If you’ve ever Googled “how to build wealth fast” or “best investments for beginners”, you’ve probably felt overwhelmed. Thousands of “gurus” and blogs claim there are hundreds of investment hacks you must follow. The truth? You only need three types of investments to build real Wealth—whether the economy is booming, crashing, or stuck sideways.

These three wealth-building pillars are:

- Income investments – so your money pays your bills (without trading time for dollars).

- Growth investments – so your net worth accelerates faster than inflation.

- Protection investments – so your Wealth survives recessions, inflation, and even global uncertainty.

This article will break down each category with examples, practical tips, and beginner-friendly strategies. We’ll also include graphs and charts so you can visualize how these three pillars work together.

Part 1: Income Investments – Making Money While You Sleep

Income investments are designed to put cash in your pocket without you physically working for it. Think of it as planting a money tree that drops fruit every season.

Why Income Matters

- Pays bills without a paycheck

- Fund lifestyle goals like travel

- Creates financial stability

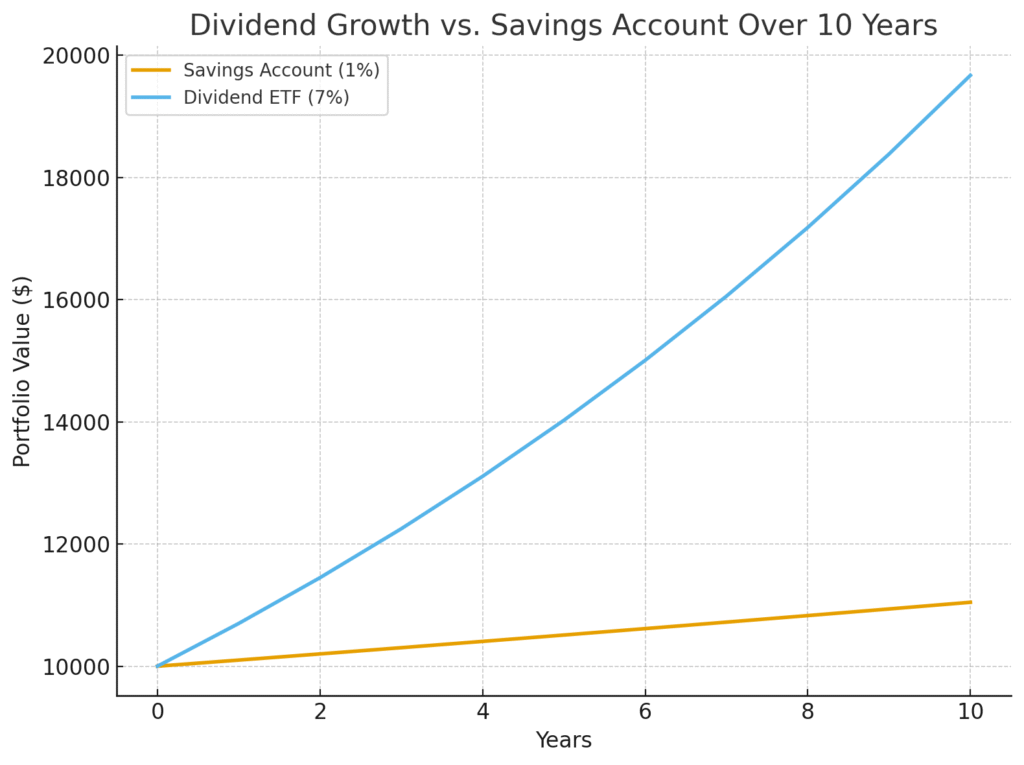

Imagine Sarah, a 35-year-old teacher. She invests $20,000 into a high-dividend ETF. That ETF pays her 4% annually, or about $800. Over time, she reinvests the dividends. Ten years later, her passive income doubles to over $1,600 annually—all without lifting a finger.

3 Ways to Generate Passive Income from Investments

1. Dividend-Paying Stocks & Funds

Instead of working for money, companies pay you a share of their profits.

Examples:

- SCHD (Schwab U.S. Dividend Equity ETF) – ~4% dividend yield

- NOBL (Dividend Aristocrats ETF) – invests in companies that have raised dividends for 25+ years

- VYMI (Vanguard International High Dividend Yield ETF) – global dividend exposure

📊 Chart: Dividend Growth vs. Regular Savings over 10 Years

2. Real Estate Rentals

Buying a rental property means tenants pay your mortgage, taxes, and leave you with extra income.

Example:

John invests $100,000 in a duplex. After expenses, it nets him $7,000 annually (a 7% return). Over time, rental income increases as property values rise.

Pros:

- Tangible asset ownership

- Tax advantages (depreciation, deductions)

- Inflation hedge

Cons:

- Requires higher upfront capital

- Active management (unless hiring property managers)

3. Cash Investments

Not all income has to be risky. Safe income sources include:

- High-yield savings accounts (4–4.5% APY in 2025)

- Certificates of Deposit (CDs) – fixed returns for locking money

- U.S. Treasuries & Treasury ETFs (like SGOV) – government-backed, low risk

While these don’t make you rich overnight, they provide a safe, predictable income.

Part 2: Growth Investments – Accelerating Your Wealth

Income pays the bills, but growth builds lasting Wealth. These investments reinvest their profits, growing your net worth faster.

Stocks for Long-Term Growth

Broad stock market funds are the easiest entry point.

Examples:

- VOO or SPY – invest in the S&P 500 (top 500 U.S. companies)

- QQQ – exposure to innovative tech companies (higher risk, higher reward)

- VUG (Vanguard Growth ETF) – large-cap growth focus

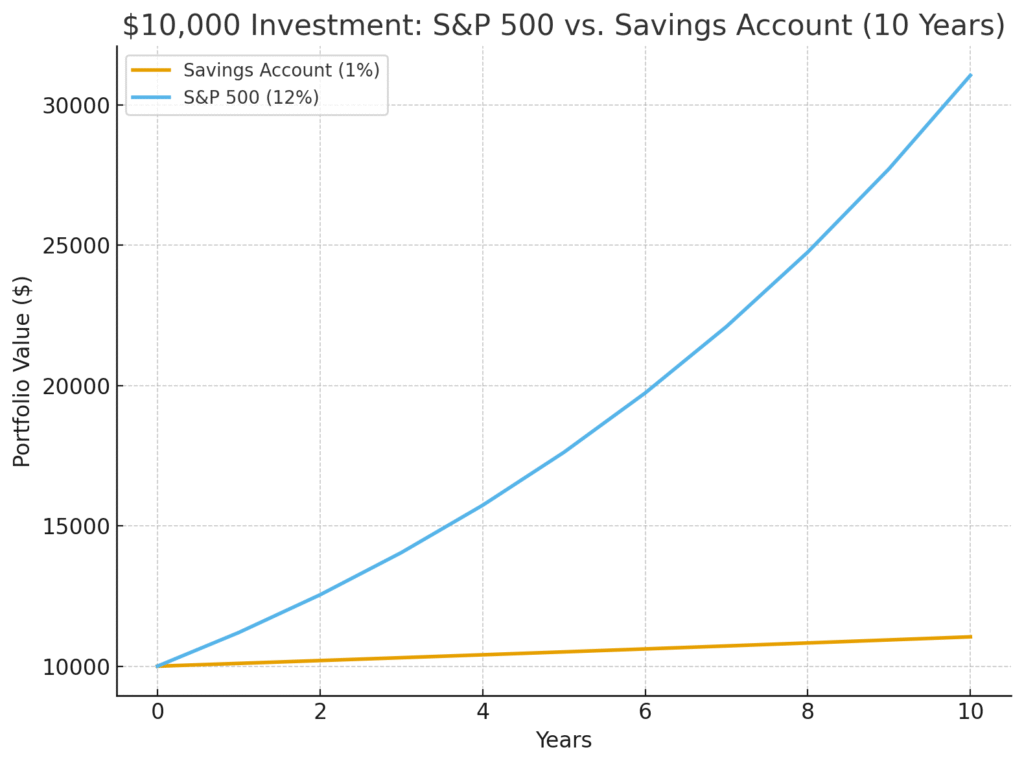

💡Example: If you had invested $10,000 in the S&P 500 in 2013, by 2023, it would be worth over $33,000—thanks to compounding growth.

📊 Graph: $10,000 Investment in S&P 500 vs. Savings Account (10 Years)

Startup Investing (High Risk, High Reward)

Platforms like Wefunder, Republic, and StartEngine allow anyone to invest in startups. While most fail, one winning investment could multiply your returns significantly.

Analogy: It’s like planting 10 seeds—most won’t sprout, but one could grow into a giant oak.

Part 3: Protection Investments – Guarding Against Recessions & Inflation

Even the best income and growth plans can collapse if you don’t protect yourself. Protection investments act as an insurance policy for your Wealth.

1. Physical Gold

Gold has preserved value for centuries. While it doesn’t generate income, it protects against inflation and currency declines.

Example: $10,000 in gold from 2010 is worth nearly $19,000 today, while the same $10,000 in cash has lost purchasing power due to inflation.

2. Bitcoin & Cryptocurrencies

Still speculative, but some investors view Bitcoin as “digital gold.” Prices swing wildly, so only allocate what you can afford to lose.

3. Foreign Market Diversification

Investing outside the U.S. shields you from domestic downturns.

- VWO (Vanguard Emerging Markets ETF) – exposure to countries like China, Brazil, and India

- EEM (iShares Emerging Markets ETF) – mid- and large-cap foreign companies

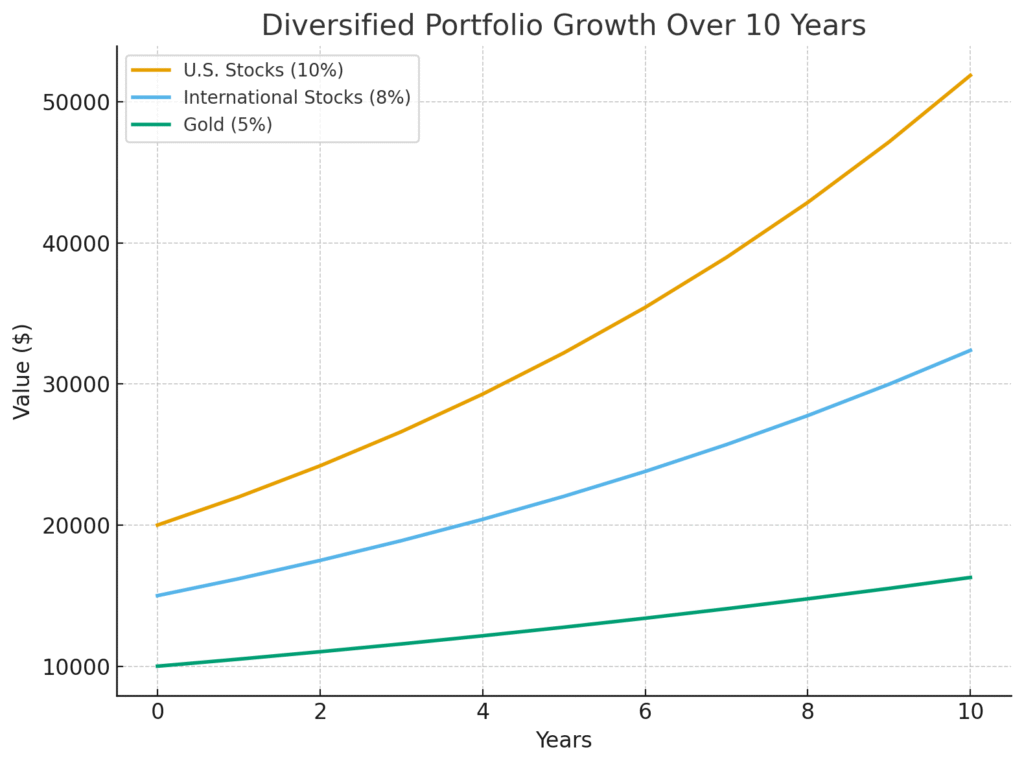

📊 Graph: Diversified Portfolio (U.S. vs. International vs. Gold) Performance

Putting It All Together: The 3-Pillar Wealth Strategy.

Here’s how a balanced portfolio might look:

| Investment Type | Allocation Example | Purpose |

|---|---|---|

| Income | 40% (Dividends, Real Estate, Cash) | Pays bills & creates stability |

| Growth | 40% (Stocks, Startups) | Builds long-term wealth |

| Protection | 20% (Gold, Bitcoin, Foreign Markets) | Shields wealth during crises |

This mix ensures you:

- Have cash flow today

- Build wealth growth for tomorrow

- Stay protected no matter the economy

Example: Building Wealth with $50,000

Let’s say Maria, a 40-year-old nurse, has saved $50,000. She could divide it as follows:

- $20,000 in dividend ETFs & rental property (income)

- $20,000 in S&P 500 & QQQ (growth)

- $10,000 in gold & international ETFs (protection)

After 10 years, her portfolio could generate steady income, solid growth, and crisis protection—without chasing every trend.

Final Thoughts

You don’t need 50 different investments or the “next hot stock” to build Wealth. By focusing on income, growth, and protection, you create a resilient, well-rounded portfolio that thrives in any economy.

Wealth isn’t built overnight—it’s built by consistent, smart decisions. Start with what you can, grow steadily, and always protect your downside.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial advice. Investing involves risk, including the potential loss of principal. Always consult with a qualified financial professional before making any investment decisions.

FAQs on Building Wealth

1. What is the safest investment for beginners?

High-yield savings accounts, CDs, and U.S. Treasuries are the safest starting points.

2. How much money do I need to start investing?

You can start with as little as $100 in ETFs or $10 in fractional shares. Real estate typically requires more capital.

3. Should I invest in crypto?

Crypto is speculative. Allocate only what you can afford to lose (typically <5% of your portfolio).

4. What’s the difference between income and growth investments?

- Income provides you with money now (in the form of dividends, rent, or interest).

- Growth builds Wealth for the future (stocks, startups).

5. Can I really build Wealth with just three investments?

Yes! By focusing on income, growth, and protection, you cover all the essential needs for wealth building without overcomplicating things.